$PAYS / @Paystreamlabs

New exploration of @MetaDAOProject's ecosystem: Paystream.

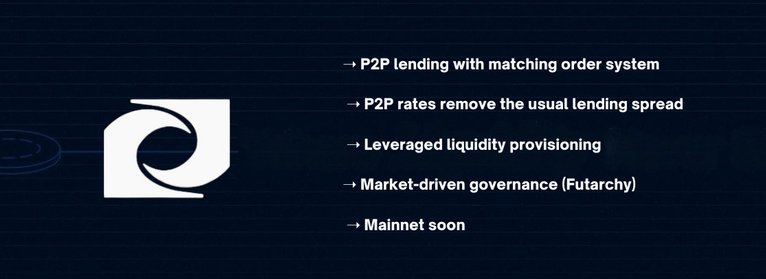

Paystream runs a P2P lending protocol on Solana that matches lenders and borrowers directly.

The system uses a leveraged engine to push APYs higher and keeps every dollar working by sending unused liquidity into the LLP (leveraged liquidity provisioning) lending pool and fallback pools.

This approach removes idle capital and keeps yields tight across the platform.

The LLP pool boosts returns on unused liquidity and keeps the overall liquidity base unified.

Paystream also lets users enter AMMs with leverage, which increases the potential returns they can generate.

There are basically 2 scenarios:

➝ When the system finds a direct match between a borrower and a lender, Paystream handles everything inside its own engine.

➝ When the engine doesn’t find a match, the liquidity moves to Kamino/Marginfi or LLP pools so the capital keeps working until a match appears.

a) If there is matching, then APY is higher

b) If no matching, your capital still works and never sits idle.

In short, Paystream allows better capital efficiency.

〖 The P2P rate

This is what I found the most interesting about Paystream as a potential user: the P2P rate.

As you probably notice, the APY spread is usually high on any lending app, and the borrow APY is usually not really favorable.

On Paystream, the spread is basically removed thanks to the matching system (borrowers and lenders positions are matched directly).

Example from Paystream documentation:

➝ Typical rates: Borrow 15% / Supply 8%

You earn 8% when you lend/supply and pay 15% when you borrow.

On Paystream, in this scenario, the P2P rate would be:

➝ APYp2p = 0.5 × 15% + 0.5 × 8% = 11.5% (for both)

➝ 11.5% when you supply and 11.5% when you borrow.

Higher returns for lenders and cheaper cost for borrowers.

Overall less friction and better UX.

Note: Paystream also offers leveraged liquidity provisioning with auto-rebalancing. I need to dig deeper and ask the team a few questions.

〖 My take:

I like the proposition from Paystream.

Big fan of lending and it's true that I've been quite often turned down by the borrow cost.

Those P2P rates could really boost usage for both lenders and borrowers.

Paystream isn't live yet (at least not publicly).

PAYS currently trades at 1.3M MC.

This looks like a very decent buy.

As you know, Paystream governance is based on MetaDAO's futarchy.

Will definitely try it when it goes live and may be tempted to add a long here.