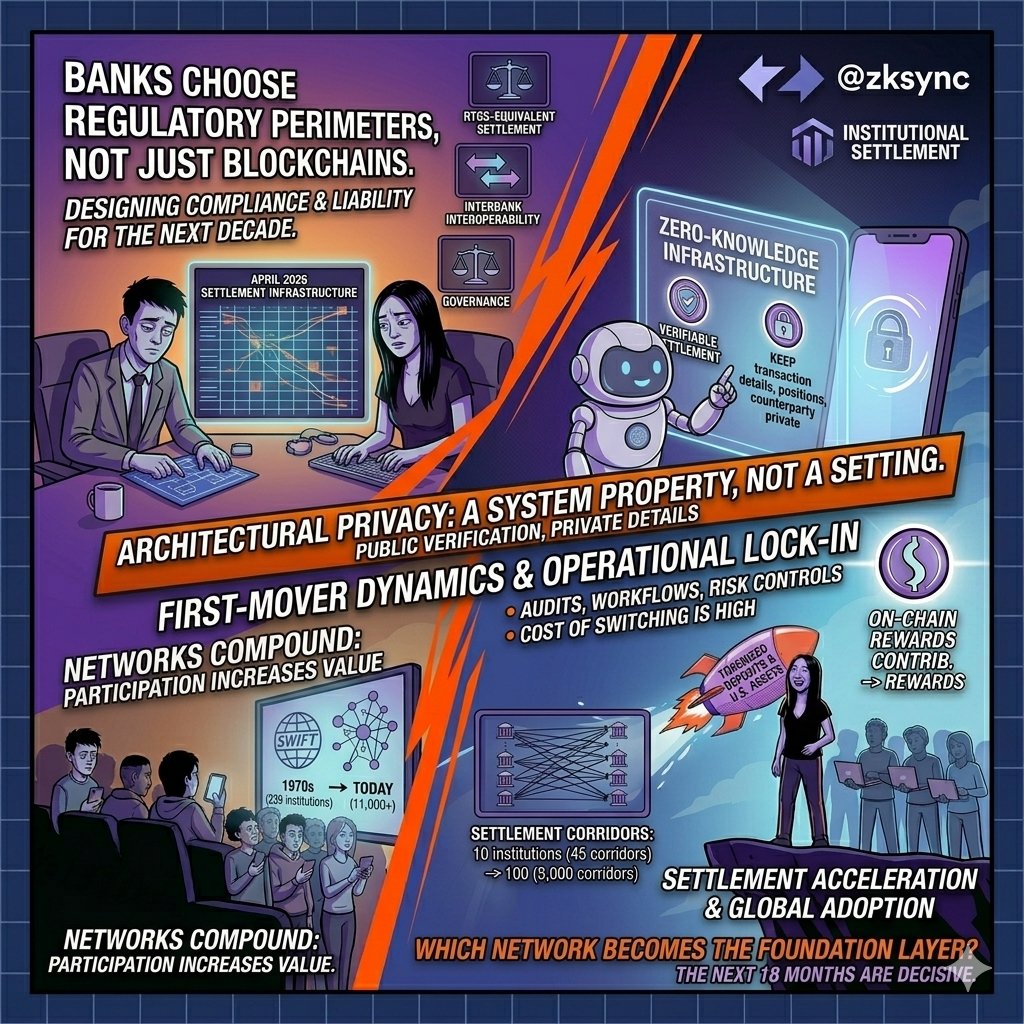

Banks aren’t choosing a blockchain. They’re choosing the regulatory perimeter they’ll operate inside for the next decade.

That’s what the 2026 settlement infrastructure decision is really about.

Right now, institutions are evaluating a set of unresolved questions that the April 2026 GFMA report identified as critical for institutional onchain finance: interbank interoperability for tokenized deposits, transaction privacy, RTGS-equivalent settlement, and governance for digital money.

These are not isolated technical features. Together, they determine whether a settlement rail can support regulated financial activity across jurisdictions.

Every rail exposes information differently. What a regulator can access, what a counterparty can infer, what an infrastructure operator can reconstruct. Those design choices shape compliance obligations, liability frameworks, and ultimately which markets a bank can operate in.

This is why privacy has become a structural issue rather than a product feature.

A privacy model that works for one jurisdiction may fail in another if confidentiality depends on permissions that can be altered later. For global institutions, privacy increasingly needs to be architectural: a property of the system itself rather than a setting that can be switched on or off.

That changes the importance of zero-knowledge infrastructure.

Instead of forcing institutions to choose between transparency and confidentiality, zero-knowledge systems allow settlement validity to be publicly verified while keeping transaction details, positions, strategies, and counterparty relationships private. Regulators can receive verifiable access without exposing sensitive information across the entire network.

For banks evaluating long-term settlement rails, that distinction matters.

The market opportunity is no longer theoretical. JPMorgan’s Kinexys platform has processed more than $1.5 trillion in transaction volume. DTCC is advancing tokenized Treasury infrastructure under existing regulatory frameworks. NYSE, BNY, and Citi are building tokenized securities rails. Meanwhile, the majority of tokenized U.S. assets already settle on Ethereum-based infrastructure.

The institutions entering these networks today are not simply choosing technology. They are helping define the standards future participants will inherit.

That is where first-mover dynamics become powerful.

Financial infrastructure compounds differently from consumer technology because adoption creates operational lock-in. Once a bank integrates a settlement rail, the costs of switching extend far beyond software migration. Institutions must repeat audits, satisfy regulators, rebuild operational workflows, renegotiate counterparty agreements, and re-establish risk controls that may have taken years to construct.

History shows how durable these effects can become.

SWIFT began with 239 institutions in the 1970s. Today it connects more than 11,000 financial institutions globally. Its dominance was not driven by superior technology alone. It persisted because every new participant increased the value of the existing network while raising the cost of choosing an alternative.

Settlement infrastructure follows the same logic.

Ten institutions create 45 potential settlement corridors. One hundred create nearly 5,000. Each additional participant increases not only transaction volume but also the number of relationships available through the network. The result is an asymmetry where the leading network's advantage compounds faster than competitors can replicate.

This is why @zksync is worth watching in the institutional race.

Its zero-knowledge architecture addresses one of the most difficult constraints identified by global financial institutions: achieving verifiable settlement while preserving confidentiality across jurisdictions. As more regulated deployments move onchain, infrastructure capable of satisfying both regulatory oversight and privacy requirements becomes increasingly valuable.

The key question is no longer whether institutional finance moves onchain.

That transition is already underway.

The question is whether privacy-preserving settlement standards can achieve sufficient adoption before regulatory fragmentation hardens into separate regional systems.

History suggests that once regulated institutions converge on a settlement standard, displacement becomes increasingly uneconomic.

The next 18 months may determine which networks become the foundation layer for institutional settlement in the decade ahead.