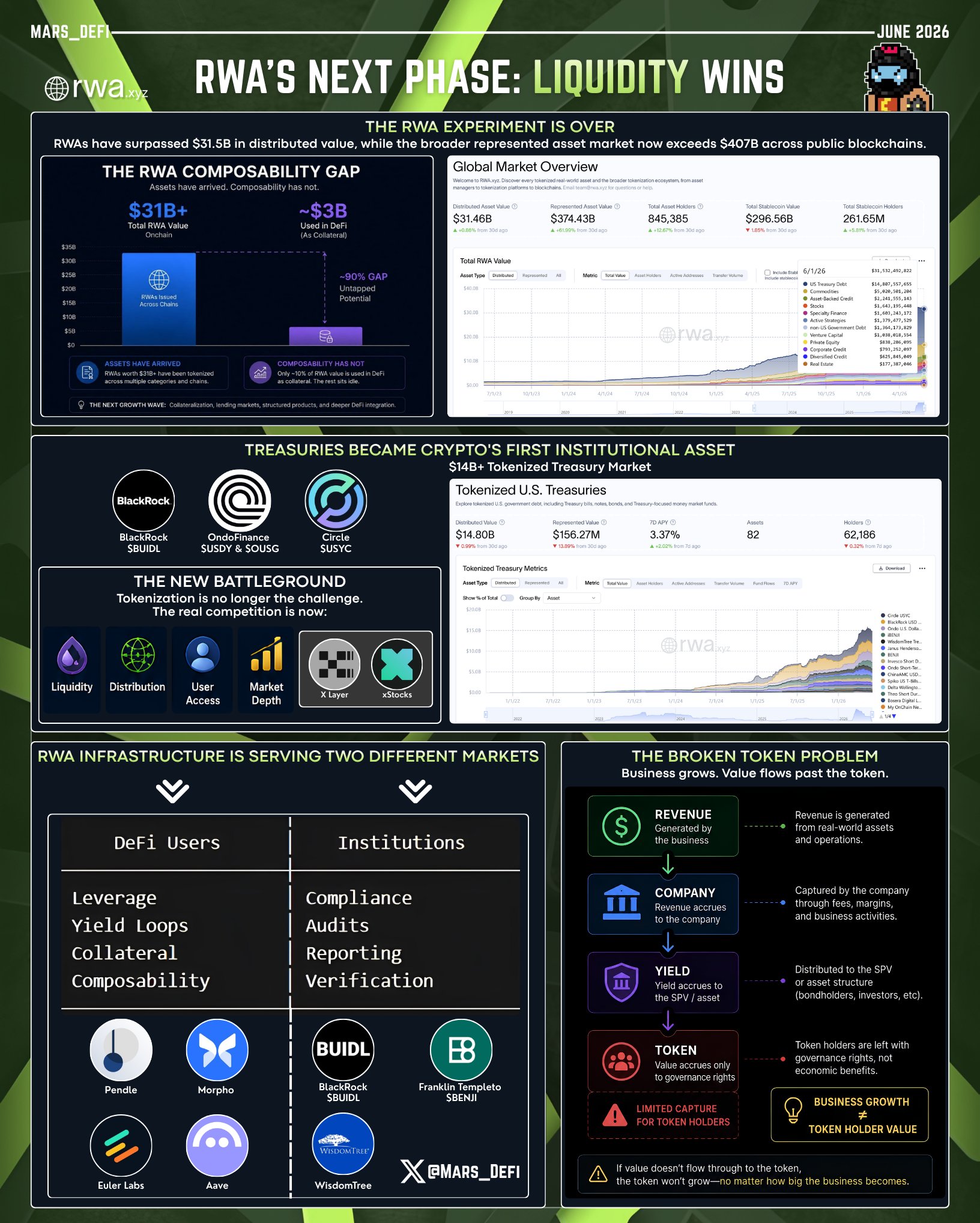

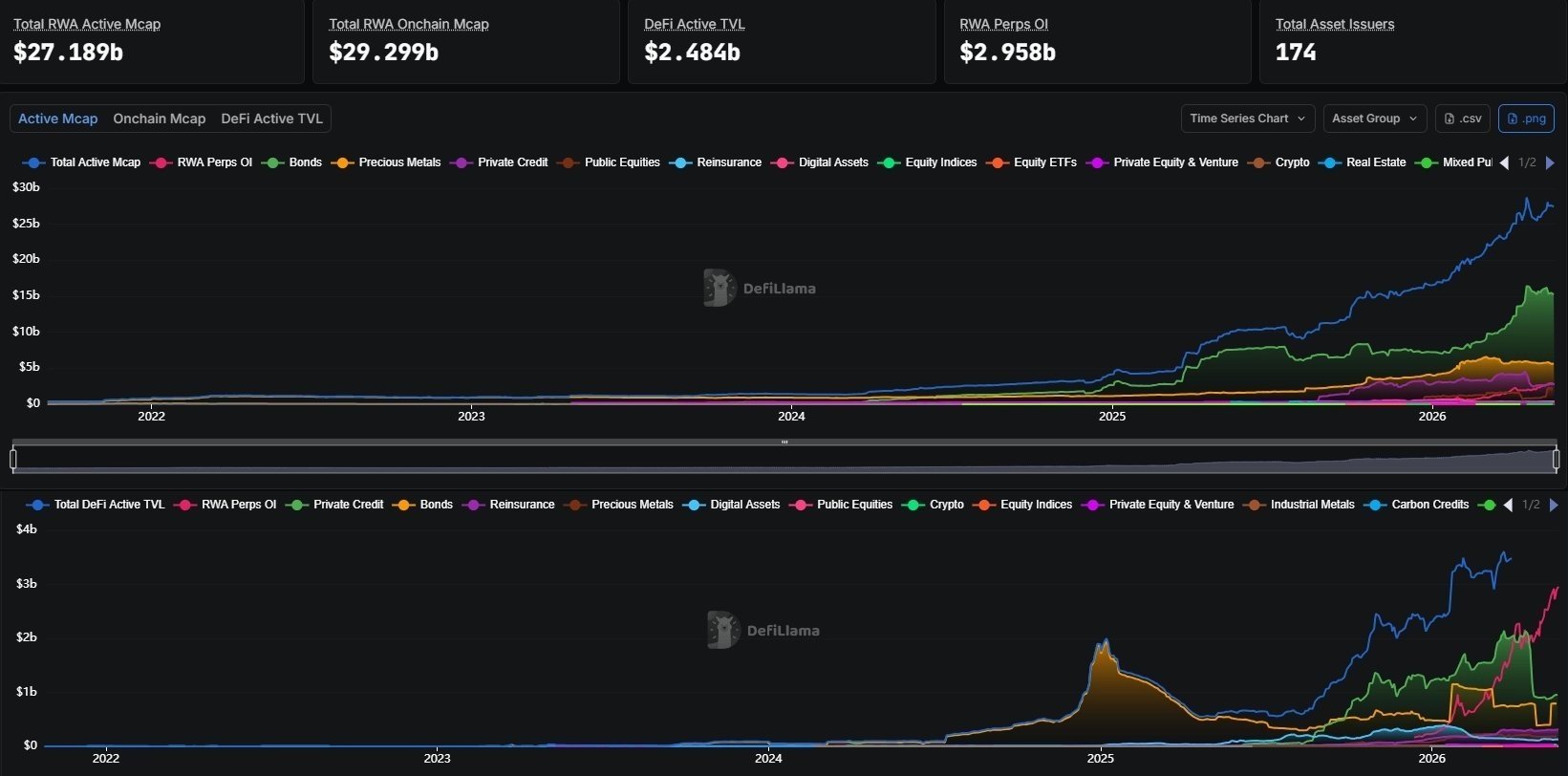

RWA value has surpassed $31.5B onchain, with tokenized stocks growing 374% and credit expanding 289% year-over-year.

Yet the most important shift is not asset tokenization itself, but the race to solve liquidity, distribution, and DeFi integration.

Here's what's actually happening:

—

● The RWA Experiment Is Over

RWAs have surpassed $31.5B in distributed value, while the broader represented asset market now exceeds $407B across public blockchains.

• Tokenized Stocks: +374% YoY

• Tokenized Credit: +289% YoY

• Commodities: +215% YoY

• Real Estate: +130% YoY

Growth is no longer coming from a single category, with capital now flowing across equities, credit, commodities, and real estate.

The industry has already proven demand for onchain assets, making infrastructure and market depth the next major battlegrounds.

—

● Why Treasuries Became Crypto's First Institutional Asset Class

Tokenized U.S. Treasuries have grown into a $14B+ market, making them the dominant gateway for institutional capital entering onchain finance.

• @BlackRock $BUIDL

• @OndoFinance $USDY & $OUSG

• @circle $USYC

Treasuries offered the ideal bridge between traditional finance and DeFi by combining familiar risk profiles, regulatory clarity, and yield-bearing exposure in an onchain format.

This is why government bonds continue to dominate RWA markets today, establishing the foundation before more complex asset classes can scale.

—

● The Next RWA Battle Is Not Asset Issuance

Tokenizing assets is no longer the hard part, as infrastructure for bringing stocks, bonds, and other real-world assets onchain already exists.

Projects like @xStocksFi and @XLayerOfficial are drawing attention because they are tackling a much bigger problem: distribution, liquidity, and user access.

Without active markets and efficient distribution channels, tokenized assets remain digitally wrapped products rather than financial assets.

Long-term winners will be determined by liquidity, distribution, and user access, not by asset issuance alone.

—

● The Largest RWA Opportunity Is Still Untapped

Despite the rapid growth of the sector, only around $3B is currently being utilized as DeFi collateral.

• ~$3B used in DeFi

• ~10% utilization

• ~90% remains outside DeFi

The largest opportunity now lies in making existing RWAs productive inside DeFi.

The assets already exist. The missing piece is composability.

—

● RWA Infrastructure Is Serving Two Different Markets

As the sector matures, RWA adoption is increasingly splitting between DeFi-native users and institutional allocators.

DeFi Users:

• Leverage

• Yield loops

• Collateral efficiency

Protocols like @pendle_fi, @Morpho, @eulerfinance, and @Aave are designed around these needs.

Institutions:

• Compliance

• Audits

• Reporting

Products such as @BlackRock's $BUIDL, @FTI_US's $BENJI, and @WisdomTreeFunds are built around these requirements.

Future RWA platforms will need to serve both groups without sacrificing composability or compliance.

—

● The Broken Token Problem

Many RWA businesses are growing, but their tokens are not.

Revenue -> Company

Yield -> Asset/SPV

Token -> Governance

Value accrues to the company and underlying assets, while token holders often capture little of it.

This creates a growing disconnect between business growth and token value.

—

The next phase of RWAs is not about tokenizing more assets, but about financializing them through lending markets, perps, vaults, RWA-backed collateral, and sustainable value accrual models.

The first phase proved that real-world assets could move onchain, while the next phase must prove they can become liquid, composable, and economically useful within DeFi.

The projects that solve liquidity, composability, and token value capture will define the next decade of tokenized finance.