Tokenized stocks are now a working market on-chain, you can trade equities like $TSLA, $NVDA, $AAPL directly on crypto rails.

What matters most is the legal structure behind each token🧵 👇

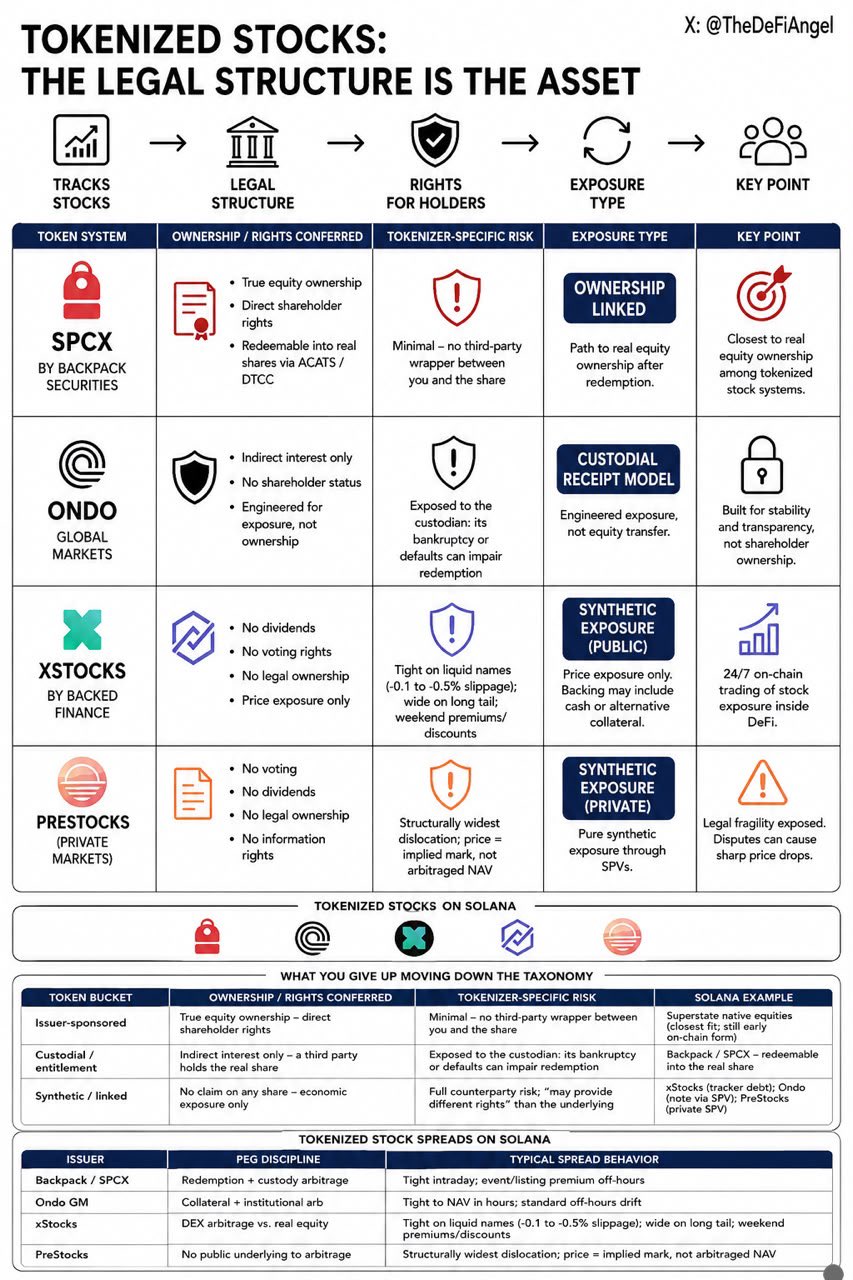

There are four major tokenized stock systems shaping this space right now:

→ Backpack Securities ($SPCX)

→ Ondo Global Markets

→ xStocks (Backed Finance)

→ PreStocks

All of them track stocks, none of them represent the same legal rights.

◢ $SPCX by @Backpack Securities sits closest to real equity ownership. It is backed 1:1 with actual shares held in regulated custody.

Qualified users can redeem tokens into real shares through traditional settlement systems like ACATS/DTCC.

That creates a direct path into real-world ownership.

Once redeemed, holders gain standard equity rights:

• dividends

• corporate actions

• transfer rights

But on-chain tokens themselves still sit inside an SPV structure until redemption happens.

◢ $Ondo Global Markets uses a structured note model that each token is backed by real securities plus additional collateral.

The structure is designed around bankruptcy-remote SPVs, independent trustees, and continuous verification.

The system is built for financial stability and transparency, but holders do not become shareholders.

There are no voting rights, no ownership claims, and no direct equity status.

The product is engineered exposure, not equity transfer.

◢ @xStocksFi by @BackedFi is designed for DeFi trading because it integrates directly into protocols like @jup_dao, @Raydium, and @kamino.

It allows 24/7 trading of stock exposure inside crypto markets, however, it does not transfer shareholder rights.

Users hold price exposure only. Dividends, voting rights, and legal ownership are not part of the structure.

In some cases, backing may include cash or alternative collateral rather than direct stock custody.

◢ @PreStocks operates in private-market exposure, it tracks companies such as @OpenAI, @AnthropicAI, and @SpaceX before IPO.

The structure is the weakest in terms of enforceable ownership.

There are no shareholder rights at all:

• no voting

• no dividends

• no legal ownership

• no information rights

Only synthetic exposure through SPVs.

In May 2026, disputes around share transfer validity triggered sharp price drops of 34–40% in affected tokens.

That event exposed the legal fragility of synthetic private exposure when underlying agreements are challenged.

Across all these systems, one important reality exists “There are two parallel price systems” which are:

• on-chain trading price (crypto markets, 24/7)

• underlying stock price (traditional markets)

Arbitrage keeps them aligned when liquidity exists, when it does not exist, gaps form and these gaps appear during weekends, low liquidity periods, and in private-market tokens.

Most trading activity is concentrated in a small set of liquid names like $TSLAx, $NVDAx, $CRCLx, $SPCX, and more

Regulators now classify tokenized stocks into three categories:

• ownership-linked instruments

• custodial receipt models

• synthetic exposure products

Each category carries different legal rights, even when the price charts look identical.

What this market is building is not just “crypto versions of stocks.” It is a split system of financial design:

» Some tokens connect to real equity ownership.

» Some are structured financial notes with collateral.

» Some are pure synthetic exposure to price movement.

→ The key point is simple:

The ticker is not the asset but the legal structure behind the token is the asset.

That is what defines what you actually hold.