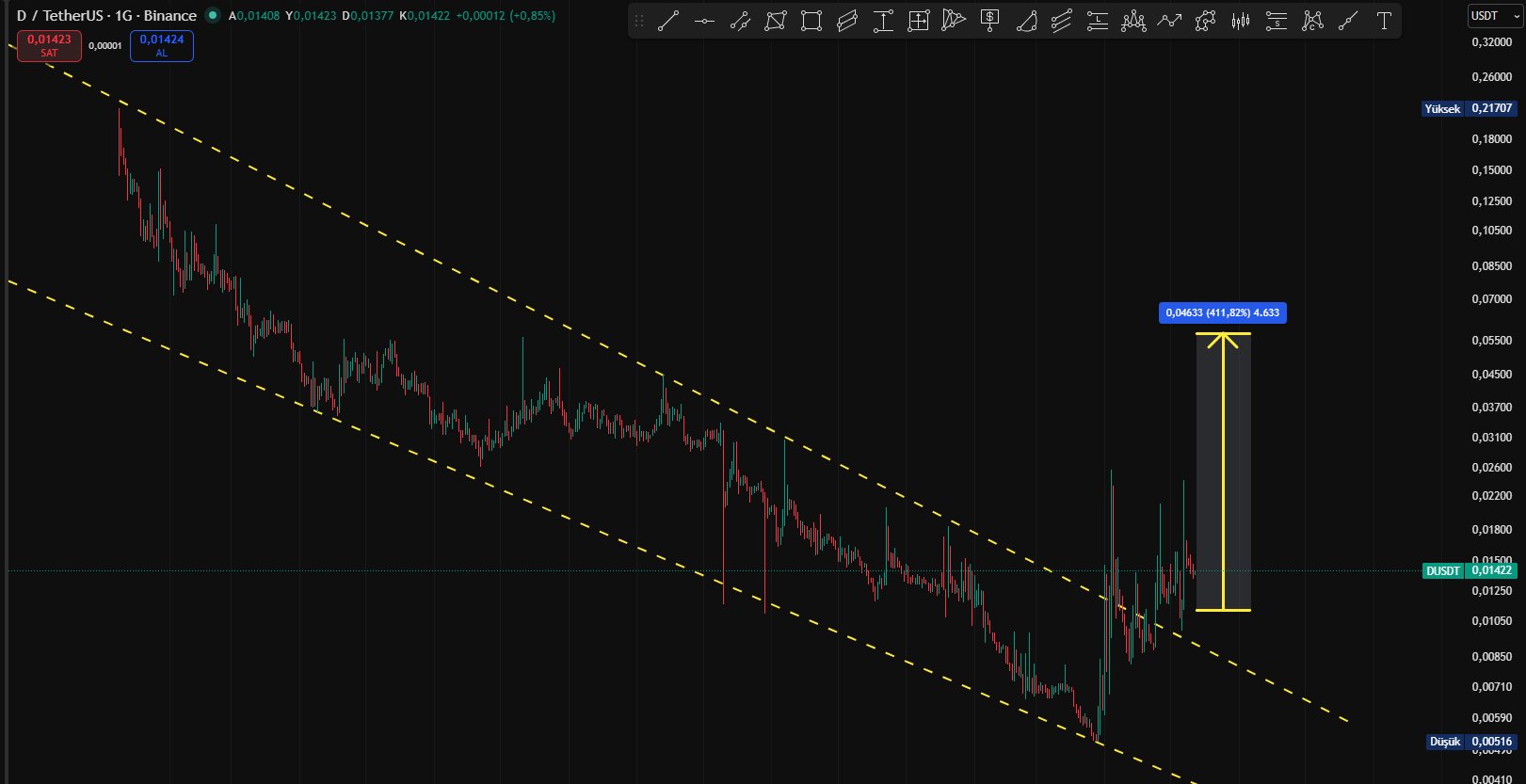

$D / #D - my high probability scenario https://t.co/GGE5ygMCkL

13.8K @ero_crypto

13.8K @ero_crypto $D / #D - my high probability scenario https://t.co/GGE5ygMCkL

6

6

0

0

935

935

27.8K @Cyriptoman4

27.8K @Cyriptoman4 $d after breaking the descending channel holds above 0.0104 and continues to accumulate at that level.

It is still difficult to give a clear directional call.

If the 0.025 $ resistance level is broken, the uptrend may continue .. https://t.co/NIxO42jh7a

79 @AhmetCa87907826

79 @AhmetCa87907826 @Cyriptoman4 Sir, could you take a look at the d coin?

76

3

2.9K

6.7K @emkfinans

6.7K @emkfinans Yes, I mentioned it on the broadcast #D struggled above resistance, broke through above $0.020 resistance and generated dollars; if it stays permanent it will run, below $0.020 risk is not taken. https://t.co/etRaz7slxp

23 @kremalimushroom

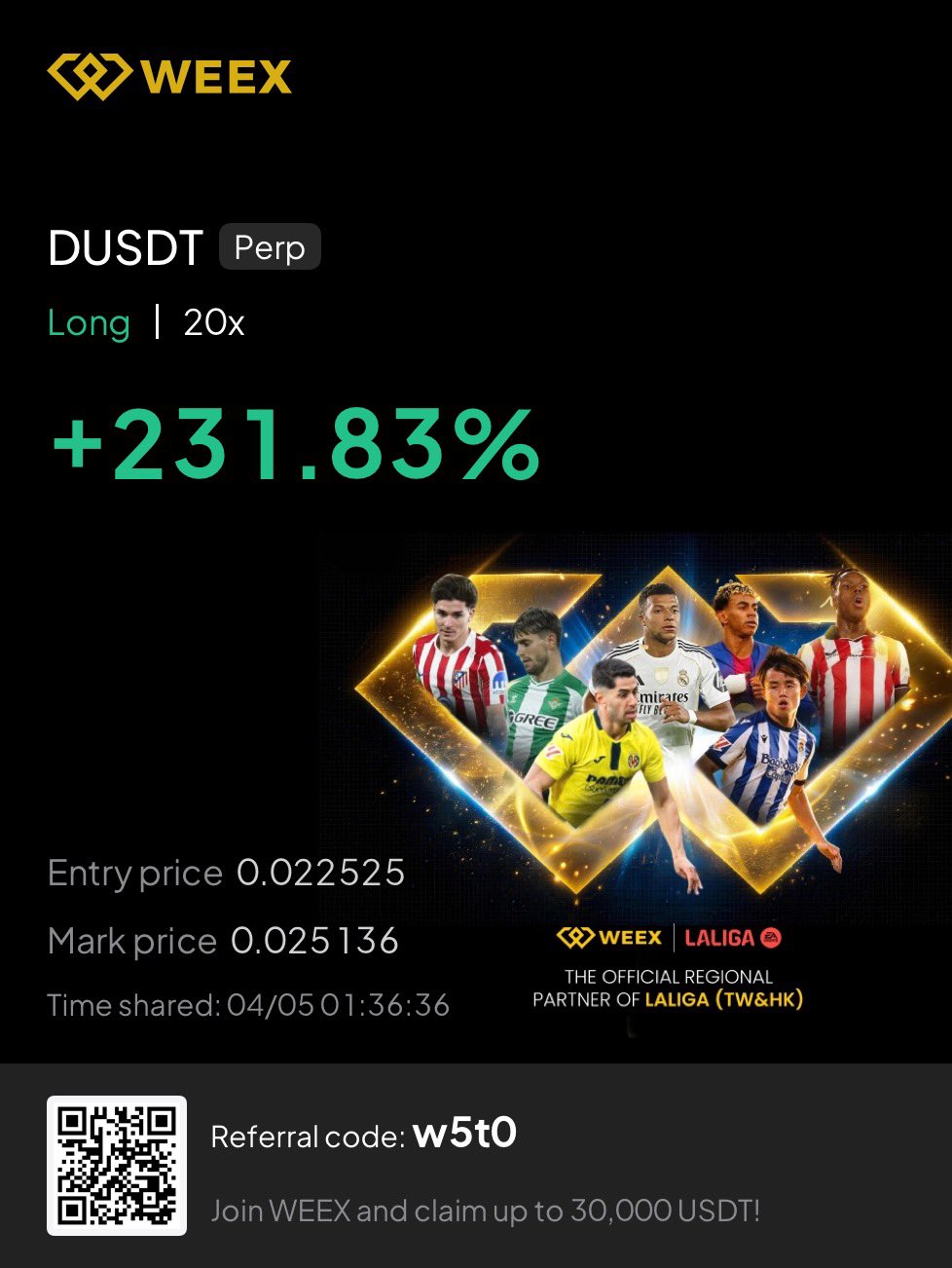

23 @kremalimushroom @emkfinans Professor, does D also reach 0.045?

24

1

1.6K